The World Bank has projected Bangladesh’s economic growth to slightly increase to 5.7% in the fiscal year 2024-25 and 5.9% in 2025/26, driven by a rise in private consumption and the implementation of large investment projects. This projection is part of the World Bank’s latest Global Economic Prospects report.

In FY 2023-24 (July 2023 to June 2024), Bangladesh’s growth is expected to slow due to elevated inflation impacting real wage growth and private consumption. Additionally, higher borrowing costs have dampened demand.

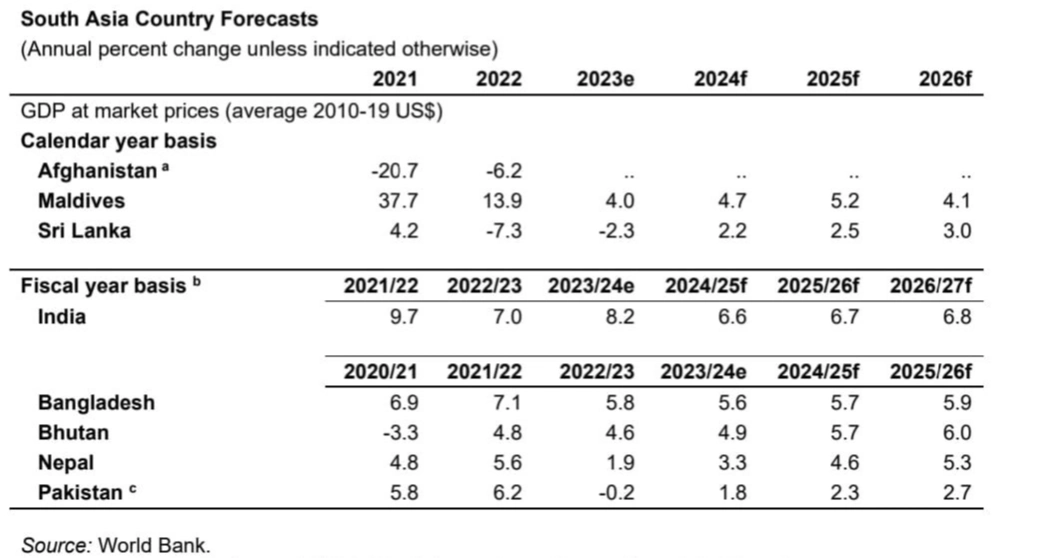

In Pakistan, economic activity, although still subdued, has shown improvement with increased industrial production in late 2023 to early 2024 following the relaxation of import controls. Growth in the South Asia region reached 6.6% in 2023, primarily fueled by faster growth in India.

Early 2024 saw mixed private sector activity across the region. While Pakistan and Sri Lanka experienced a pickup, Bangladesh faced disruptions in industrial activity due to ongoing import restrictions.

India`s growth in FY2023-24 (April 2023 to March 2024) was bolstered by stronger-than-expected industrial and services activity, despite a slowdown in agricultural production caused by monsoons.

Sri Lanka saw an economic boost from recovering tourism and remittances, although both remained below pre-pandemic levels. Bhutan and Nepal are also poised for growth, partly due to recoveries in tourism and remittances.

Growth in the South Asia region is forecasted to slow to 6.2% in 2024 and remain at that rate through 2025-26, with steady growth expected in India.

Globally, the economy is anticipated to stabilize in 2024 for the first time in three years, with growth holding steady at 2.6% before increasing slightly to 2.7% in 2025-26. This remains below the pre-COVID-19 decade average of 3.1%.

Developing economies are projected to grow at an average rate of 4% over 2024-25, slightly slower than in 2023. Low-income economies are expected to see growth accelerate to 5% in 2024 from 3.8% in 2023. However, three-quarters of these economies have had their 2024 growth forecasts downgraded since January.

In contrast, advanced economies are projected to maintain steady growth at 1.5% in 2024, rising to 1.7% in 2025.

World Bank Insights on Global Economic Challenges

"Four years after the upheavals caused by the pandemic, conflicts, inflation, and monetary tightening, it appears that global economic growth is steadying," said Indermit Gill, World Bank Group’s Chief Economist and Senior Vice President. "However, growth is at lower levels than before 2020. Prospects for the world’s poorest economies are even more worrisome. They face punishing levels of debt service, constricting trade possibilities, and costly climate events. Developing economies will have to find ways to encourage private investment, reduce public debt, and improve education, health, and basic infrastructure."

One in four developing economies is expected to remain poorer than in 2019. The income gap between developing and advanced economies is set to widen in nearly half of developing economies over 2020-24, the highest share since the 1990s. Per capita income growth in these economies is expected to average 3.0% through 2026, below the pre-COVID-19 average of 3.8%.

Global inflation is projected to moderate to 3.5% in 2024 and 2.9% in 2025, but the decline is slower than previously expected. Many central banks are likely to keep interest rates high, averaging about 4% over 2025-26, double the 2000-19 average.

The Global Economic Prospects report highlights the importance of public investment in accelerating private investment and promoting economic growth. It suggests that increasing public investment by 1% of GDP in developing economies could boost output by up to 1.6% over the medium term.

The report also addresses the fiscal challenges faced by small states, emphasizing the need for comprehensive reforms to improve revenue stability, spending efficiency, and fiscal frameworks.

-20260803102832.webp)